May 5, 2026

CVS Health: One Number Will Define Wednesday’s Move

Q1 2026 earnings hit pre-market May 6. The Aetna medical benefit ratio is the only line that matters — everything else is noise.

☰

Dear Fellow Investor,

Let me give you a number.

90 to 1.

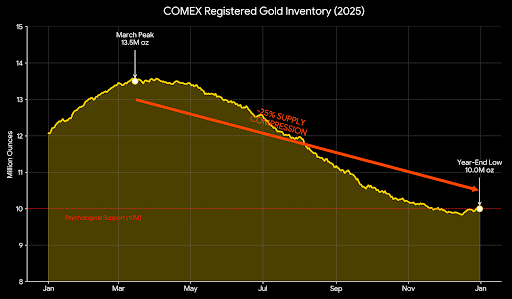

That’s how many paper gold claims exist for every real ounce in COMEX vaults.

Ninety promises. One ounce of metal.

It’s like a game of musical chairs. Except there are 90 players. And only 1 chair.

When the music stops, 89 people lose.

COMEX gold inventory dropped 25% last year alone. The gold is flowing East. Shanghai. Mumbai. Moscow.

On May 29th, contract holders can demand delivery. If too many show up at once…

You’ve seen what happens. They change the rules. They close markets. They ban buying.

Every time, paper holders got crushed. Mining stock holders made fortunes.

I’ve found the one stock at the center of this crisis.

Get the name and ticker here >>>

“The Buck Stops Here,”

Dylan Jovine, CEO & Founder

Behind the Markets

FEATURED

CVS Health: One Number Will Define Wednesday’s Move

Let’s start with where we actually are. CVS Health touched $58.35 on May 15, 2025. As of Tuesday’s close it was near $82. That’s a 40% recovery off the trough — and it happened without a single transformational business event. No spinoff, no buyout rumor, no blowout quarter. What moved this stock was a slow drip of less-bad news on Aetna’s medical costs, a favorable CMS rate decision in April, and the quiet realization that the asset base was never the problem.

Wednesday morning, before the open, that narrative gets its first real stress test of 2026. Q1 earnings. And what comes out of the Aetna segment — specifically the medical benefit ratio — will either validate the recovery trade or reopen a debate that most of the Street thought was settled.

Here’s the setup in full.

Why This Name Got Destroyed — and Why It Came Back

The bear case on CVS from 2023 through mid-2025 was specific: Aetna’s Medicare Advantage book was bleeding. Post-pandemic utilization — more surgeries, more specialist visits, more deferred care coming due — hit the MA segment faster and harder than anyone modeled. The medical benefit ratio, which measures what percentage of premiums goes to actual medical claims, ran at 92.5% for full-year 2024. Anything above 87–88% in Medicare Advantage is a margin problem. At 92.5% it was close to an existential one.

CVS cut guidance twice in 2024. Replaced the CEO. Took a $5.7 billion goodwill impairment on Oak Street Health in Q3 2025. GAAP EPS for the full year came in at $1.39. The stock, which had traded near $95 in 2022, got cut almost in half.

What changed was deliberate. Management pulled back from unprofitable Medicare Advantage counties — a choice that cost 504,000 members by year-end 2025 but improved the underlying risk pool. CostVantage, the pharmacy’s shift to cost-based reimbursement, completed its rollout across commercial, Medicare, and Medicaid lines, removing a structural pharmacy margin drag that had been in place for years. And on April 7, CMS finalized 2027 Medicare Advantage rates at a net increase of approximately 2.48% — over $13 billion in additional industry funding, far above the 0.09% rate that had briefly rattled the sector in January. CVS gapped 9%+ after hours on that news alone.

Full-year 2025 adjusted EPS came in at $6.75 — beating the original $5.75–$6.00 guidance range by roughly 15%. Operating cash flow hit $10.6 billion, above management’s own updated expectations. The MBR improved from 92.5% to 91.2% for the full year. Still above target. But the direction is what matters.

The Snapshot

- Current price: ~$82 | 52-week range: $58.35–$85.15

- Market cap: ~$105.1B | Shares outstanding: 1.28 billion

- 2025 full-year revenue: $402.1 billion (up 7.8% YoY — a record)

- 2025 adjusted EPS: $6.75 | GAAP EPS: $1.39 (impairment-distorted)

- 2026 adjusted EPS guidance: $7.00–$7.20 | Cash flow guidance: $9.0B+

- Q1 2026 EPS consensus: ~$2.21–$2.23 | Revenue consensus: ~$94.37–$95.28B

- Forward P/E (NTM): ~11.4x | Dividend yield: 3.24% ($0.665/quarter)

- Analyst consensus target: $94.95–$96.58 | 20 of 24 analysts rated Strong Buy

- Beta: 0.60 | Avg daily volume: ~7–8 million shares

Hidden in Tesla’s Filing: A $12 Billion “Super Startup”

Pull up Tesla’s most recent SEC filing. Page 5.

And you’ll see a single line showing $12 billion in revenue from a brand-new “super startup” Elon Musk has been quietly incubating inside Tesla.

This new “super startup” has nothing to do with cars or robots or space or AI…

But it sits at the center of what Blackstone calls “a $23 trillion investment opportunity.”

And on July 22, Elon is expected to pull back the curtain and reveal exactly what he’s building.

But Adam O’Dell already knows… and he reveals it all in this urgent video.

☰

Three Businesses. One Problem Segment.

CVS operates as three distinct revenue engines, and traders who blur them together tend to misread both the upside and the downside.

Health Care Benefits (Aetna) is the swing factor — and the reason this stock has been a two-year rollercoaster. Full-year 2025 revenues came in at $143.4 billion, up from $130.7 billion in 2024. The MBR improved from 92.5% to 91.2% year-over-year. Aetna’s adjusted operating income improved by more than $2.6 billion versus 2024. Management is targeting 3–5% Medicare Advantage margins — they’re not there yet, but the trajectory is right. Over 81% of Aetna’s MA members are enrolled in plans rated 4 stars or higher for 2026, which matters for CMS bonus payment eligibility. The Q1 2025 comparable MBR was 87.3% — so the bar Wednesday sets is whether Aetna is running near that level or running hot again.

Health Services (Caremark) is the quiet engine that doesn’t get enough credit. Full-year 2025 revenues came in at $190.4 billion, up from $173.6 billion — a 9.7% increase. The 2025 selling season closed with nearly $6 billion in contract wins and retention above 98%. The TrueCost transparent pricing model aligns well with the direction of incoming PBM legislation, which is pushing the industry toward pass-through structures. This segment is predictable, sticky, and consistently cash-generative. It’s also the reason CVS doesn’t deserve to trade at a distressed multiple.

Pharmacy and Consumer Wellness is stabilizing. Prescription volume grew 5.4% on a 30-day equivalent basis in 2025. Script share nationally sits near 29%. The Rite Aid prescription file acquisition brought in approximately 9 million new patients. Q1 2026 segment revenues are expected to grow around 9.8% year-over-year. The retail front-of-store business — the old albatross — has been largely deprioritized. CVS is pivoting toward pharmacy-only formats, with nearly 20 smaller-footprint locations and over 40 new pharmacies planned for 2026. The transformation isn’t glamorous, but it’s directionally sound.

The Valuation Gap Worth Understanding

The TTM P/E of ~59x is a distortion, not a data point. It reflects the $5.7 billion Oak Street Health goodwill impairment taken in Q3 2025, which crushed reported GAAP EPS to $1.39 for the full year. The number that actually describes CVS’s earnings power is the forward P/E — approximately 11.4x on the $7.00–$7.20 adjusted EPS guidance range.

UnitedHealth Group historically trades at 15–20x forward. Humana, with a more impaired MA book, still commands a premium to where CVS sits. If CVS simply re-rates to 13x on the $7.10 midpoint — not a stretch given Caremark’s scale and the CostVantage transition — that’s a stock in the $92–$99 range. The analyst community is already there: consensus 12-month target sits at $94.95–$96.58, with Wolfe Research at $100 and Piper Sandler at $99 on the high end. Twenty of 24 tracked analysts rate it Strong Buy or equivalent.

Management’s own 3-year target is mid-teens adjusted EPS CAGR through 2028. That math requires consistent Aetna margin recovery. Which is why Wednesday matters more than a typical quarter.

Chart Structure Going Into the Print

The 52-week high of $85.15 was set on October 29, 2025 — the day CVS reported Q3 earnings. That level hasn’t been reclaimed since. The stock has been consolidating the April CMS catalyst move in the $80–$83 zone, RSI hovering around 62, volume normalizing. It’s a coiling pattern. Earnings are the release valve.

- Immediate resistance: $82.52–$83.87 — the consolidation ceiling the stock keeps running into

- Key breakout level: $85.15 — reclaiming the 52-week high on volume would bring in momentum buyers

- First support: $78 — a close below here signals the post-CMS move is being fully unwound

- Structural support: $70.08–$70.48 — multi-timeframe trend line confluence; this is where long-term buyers step in if the thesis breaks

- 200-day SMA: ~$72–$73 — former resistance, now acts as a floor on meaningful pullbacks

The setup is clean in the sense that the levels are defined. The chop zone is $80–$83. A beat with any guidance raise — even a subtle tightening toward the high end of $7.00–$7.20 — breaks the stock through resistance and potentially tags $88–$90 in the sessions following. A miss, or worse, cautious medical cost language from management, puts $78 back in play fast. Those two scenarios look about equidistant from where the tape is right now.

☰

Sector Backdrop — What the Peer Prints Already Told Us

Before getting to the scenarios, one tangent worth sitting with: the managed care read-through has been mixed-to-positive. Centene delivered 7.1% Q1 revenue growth and beat estimates by 6.2% — shares jumped 24%. Elevance came in with revenues up 1.5%, beating by 2.4%, up 5.5% post-report. Health insurance names in aggregate have averaged a 5.7% share price gain over the past month. The sector is not broken.

That’s constructive for CVS — but it also means expectations have already moved. The stock is already pricing in a recovery. Wednesday’s question isn’t whether CVS can bounce. It’s whether the fundamentals have caught up to the price.

Three Scenarios

Bull — Aetna MBR comes in below 88%. Q1 EPS beats the $2.21–$2.23 consensus. Management tightens guidance toward the high end of $7.00–$7.20, or formally raises. Call commentary is constructive on 2027 MA margin trajectory given the locked-in CMS rate increase. Stock breaks above $85.15 on volume — new 52-week high, momentum buyers engage. Near-term target: $90–$100. Twelve-month target: $100+ at 13–14x $7.10 midpoint EPS. CVS has beaten consensus EPS in each of the last four quarters with an average surprise of 20.6%, so a beat itself wouldn’t be a shock — the variable is whether guidance moves.

Base — modest beat, reaffirmed guidance. EPS beats narrowly. Revenue comes in near or slightly below the $94.37B estimate — partly by design, given the deliberate Aetna membership pullback. Management reaffirms $7.00–$7.20 without raising. Medical cost language is cautious but not alarming. Stock grinds higher over the following weeks toward $85–$88 without a big session move. The re-rating continues on a slower timeline. This is probably the most likely outcome, and for existing longs it’s fine — just not exciting.

Bear — utilization trends resurface. Elevated medical costs — flu, GLP-1 specialty drug spend, or Medicare Part D seasonality under the Inflation Reduction Act — push Aetna’s Q1 MBR back above 89–90%. EPS misses. Management either guides cautiously or explicitly pushes target margin recovery into 2027. The post-CMS gains unwind. Any new Oak Street Health charges or clinic closure announcements would compound the damage. First stop: $78 — watch for a decisive close below that level. Structural support at $70–$75 comes back into play. Full-year guidance cut below $7.00 adjusted EPS would force a thesis re-evaluation.

Elon’s $480 Trillion Currency Masterplan

He’s waited 27 years for this moment. Elon Musk just launched his biggest disruption ever, which could totally reset how millions of people access their money and even pay tax.

How to Trade It

CVS options have been running elevated implied volatility into this print — unusual call volume was flagged in late April, and the directional lean in the options market has been bullish. The CMS catalyst showed the stock can gap 9–10% on a macro event. Expect the implied move to be wider than the 0.60 beta would normally suggest. Check pre-market options pricing Wednesday before making any move.

- Already long? The defined stop is a close below $78. That’s roughly 5% from Tuesday’s close and a level that signals the market is rejecting the recovery narrative at current valuations. Respect it.

- Looking to enter long? Don’t chase into the print. Wait for the number. A beat with guidance raise, confirmed by a hold above $83 in the first 30 minutes post-open, is a cleaner setup than going in blind the night before.

- Playing volatility? The wider-than-normal implied move creates opportunities in both directions. Know the strikes, know the cost of carry, and size accordingly for a 0.60 beta name — this is not a momentum vehicle.

- Longer-term positioning: The $10.6 billion in 2025 operating cash flow, Caremark’s $190B revenue base, and the CMS rate tailwind are real. The floor under the thesis is durable. But the re-rating from 11x to 13–14x forward requires multiple quarters of clean Aetna execution — not just one.

- Peer benchmarks: UNH near $370 at 15–16x forward. HUM near $236 with a more impaired MA book. CVS at 11x, with an improving MBR trajectory and a $9B+ annual cash flow engine, is still the cheapest name in large-cap managed care.

What’s interesting is that CVS at $82 is not the same trade it was at $58. The easy money has already been made. What’s left is a re-rating story that requires the company to prove, quarter by quarter, that Aetna’s 2024 blowup was a cyclical problem and not a structural one. Wednesday is the first real data point of 2026 on that question.

One thing that doesn’t get said enough: CVS threw off $10.6 billion in operating cash in 2025 — a year that included a $5.7 billion goodwill write-down and two CEO transitions in three years. The cash generation is real even when the headlines are ugly. That’s the part of the story that keeps 20 of 24 analysts at Strong Buy. It’s also the part that makes the floor feel credible, even in a bear scenario.

One number. Wednesday morning. Aetna’s MBR.

For informational and educational purposes only. Not investment advice. Trading involves risk, including possible loss of principal.